IRS Lifetime Gift Tax Exemption 2025: A Comprehensive Guide

Related Articles: IRS Lifetime Gift Tax Exemption 2025: A Comprehensive Guide

- The Nissan GT-R: A 2500 HP Beast Of Speed And Engineering

- FAFSA Sign In As Parent 2025: A Comprehensive Guide For Parents

- Dodge Stealth Engine Bay: A Comprehensive Guide To The Intricate Architecture Of A Performance Icon

- 2025 Subaru Forester Touring: A Comprehensive Overview

- The Newest Dodge Viper: A Return To The Golden Age Of American Muscle

Introduction

With great pleasure, we will explore the intriguing topic related to IRS Lifetime Gift Tax Exemption 2025: A Comprehensive Guide. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Video about IRS Lifetime Gift Tax Exemption 2025: A Comprehensive Guide

IRS Lifetime Gift Tax Exemption 2025: A Comprehensive Guide

Introduction

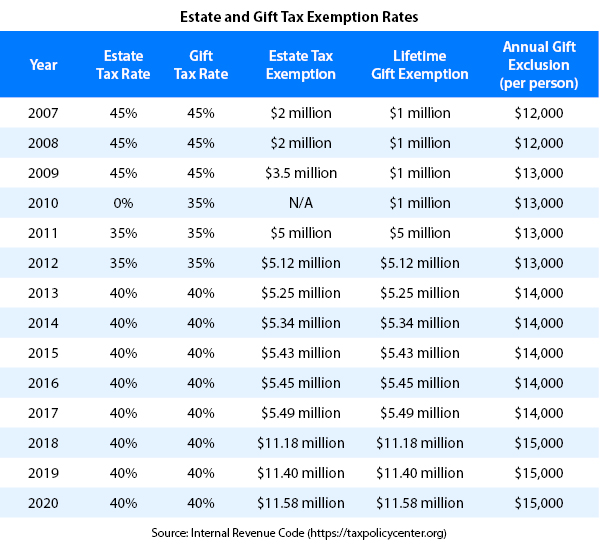

The Internal Revenue Service (IRS) imposes a tax on individuals who make gifts exceeding certain thresholds. The lifetime gift tax exemption is the maximum amount an individual can give away during their lifetime without incurring any gift tax liability. This exemption amount is adjusted periodically to keep pace with inflation. The current lifetime gift tax exemption is $12.06 million for 2023 and 2024. However, this exemption is set to decrease significantly in 2025.

The 2025 Gift Tax Exemption

Under the Tax Cuts and Jobs Act (TCJA) of 2017, the lifetime gift tax exemption was temporarily doubled to $12.06 million. This increase was originally set to expire on December 31, 2025. However, the Consolidated Appropriations Act of 2023 extended the increased exemption through 2025.

After December 31, 2025, the lifetime gift tax exemption will revert to its pre-TCJA level of $5 million, adjusted for inflation. The current inflation-adjusted exemption for 2026 is $6.29 million.

Impact of the Lower Exemption

The reduction in the lifetime gift tax exemption will have a significant impact on individuals who plan to make substantial gifts during their lifetime. Gifts made in excess of the exemption amount will be subject to a gift tax rate of up to 40%.

For example, if an individual makes a gift of $7 million in 2026, they will be subject to a gift tax of $800,000. This is because the gift exceeds the exemption amount of $6.29 million by $700,000. The gift tax rate of 40% is applied to the excess amount, resulting in a tax liability of $800,000.

Planning for the Lower Exemption

Individuals who plan to make substantial gifts should consider taking steps to minimize their gift tax liability in light of the lower exemption. Some strategies to consider include:

- Making gifts before 2026: Individuals who plan to make large gifts may want to consider doing so before the lifetime gift tax exemption reverts to a lower level in 2026.

- Using the annual exclusion: The annual exclusion allows individuals to make gifts of up to $17,000 per year to any number of recipients without incurring any gift tax liability. Individuals can take advantage of this exclusion by spreading their gifts over multiple years.

- Using trusts: Trusts can be used to reduce gift tax liability by allowing individuals to transfer assets to a trust for the benefit of others. Trusts can also be used to shelter future appreciation in value from gift tax.

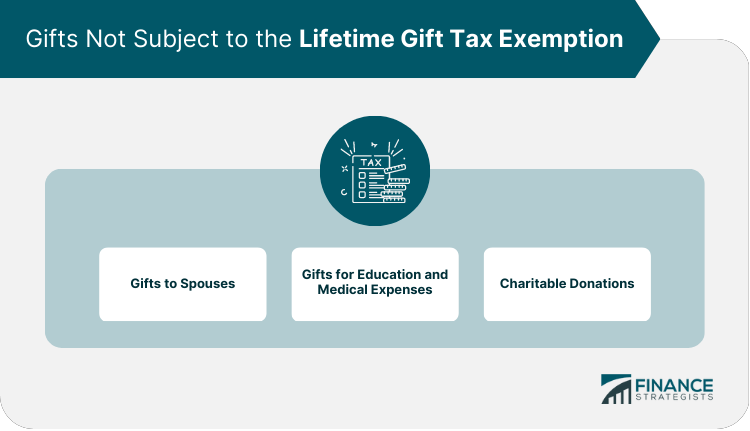

- Making charitable gifts: Gifts to qualified charities are not subject to gift tax. Individuals can use charitable giving to reduce their overall gift tax liability.

Conclusion

The lifetime gift tax exemption is a significant factor to consider when planning for the transfer of assets during one’s lifetime. The scheduled reduction in the exemption in 2026 will have a major impact on individuals who plan to make substantial gifts. By understanding the exemption and the strategies available to minimize gift tax liability, individuals can effectively plan for the future and preserve their wealth.

Additional Information

- The lifetime gift tax exemption is a federal exemption. State gift tax laws may vary.

- The gift tax exemption is not indexed for inflation after 2025.

- Gifts made to a spouse who is a U.S. citizen or resident are not subject to gift tax.

- The gift tax exemption is not affected by the estate tax exemption.

- Individuals should consult with a qualified tax professional for personalized advice on gift tax planning.

Closure

Thus, we hope this article has provided valuable insights into IRS Lifetime Gift Tax Exemption 2025: A Comprehensive Guide. We thank you for taking the time to read this article. See you in our next article!